Great Strong Advice Concerning House Mortgages That Anybody Can Use

Content create by-Napier PruittSigning the papers for your first home mortgage is an exciting event. But, before you sign those papers, you have to make sure you are getting a fair deal on your mortgage. This article can help you with this endeavor. Remember the tips below when you are negotiating terms for your home mortgage.

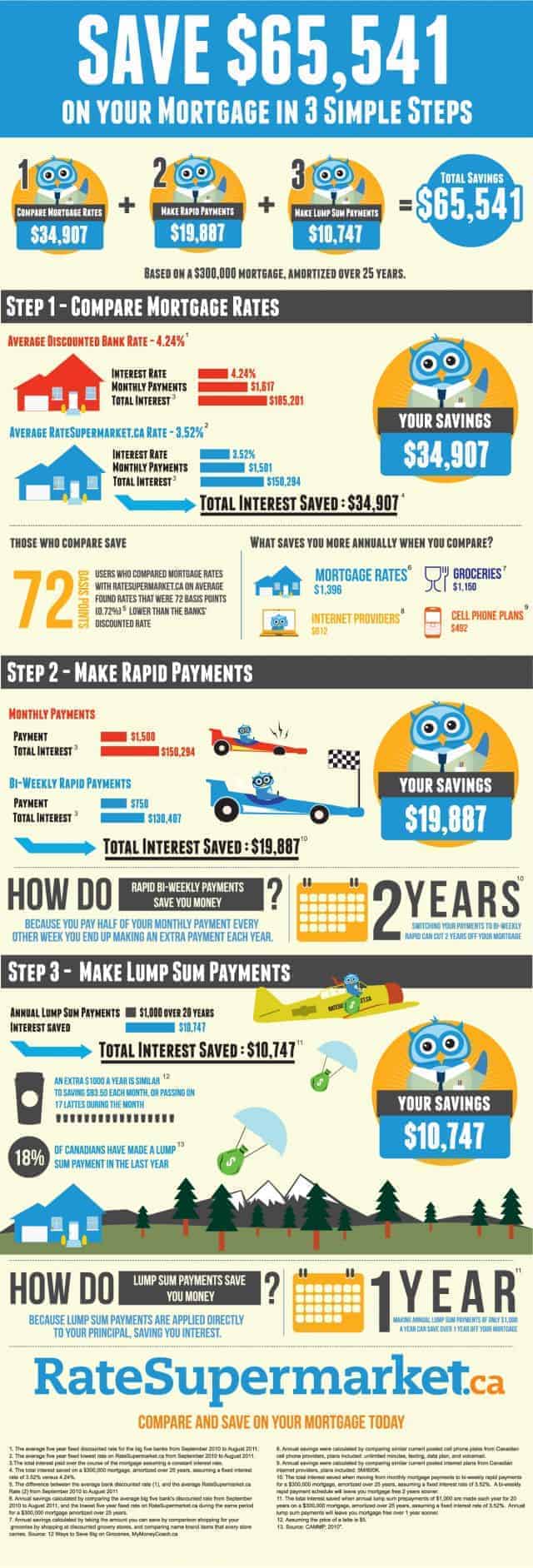

If the idea of a mortgage looming over your head for the next few decades does not appeal to you, consider refinancing over a shorter period. Although your monthly payments will be more, you'll save a lot in terms of interest over the life of the loan. It also means being mortgage-free much sooner, and owning your home outright!

If you want a good mortgage, you should have an excellent work history. In https://www.pymnts.com/news/banking/2021/bank-independent-how-banks-can-tap-a-la-carte-business-model-engage-smbs/ , it's the norm for a home lender to expect buyers to have been in their job position for two or more years. Having too many jobs in a short period of time may make you unable to get your mortgage. You should never quit your job during the application process.

If you are planning on purchasing a house, make sure your credit is in good standing. Most lenders want to make sure your credit history has been spotless for at least a year. To obtain the best rate, your credit score should be at least 720. Remember that the lower your score is, the harder the chances of getting approved.

Hire an attorney to help you understand your mortgage terms. Even those with degrees in accounting can find it difficult to fully understand the terms of a mortgage loan, and just trusting someone's word on what everything means can cause you problems down the line. Get an attorney to look it over and make everything clear.

Obtain a credit report. It is important to understand your credit rating before you begin any financial undertaking. Order reports from all 3 of the major credit reporting agencies. Compare them and look for any erroneous information that may appear. Once you have a good understanding of your ratings, you will know what to expect from lenders .

Try to have a down payment of at least 20 percent of the sales price. In addition to lowering your interest rate, you will also avoid pmi or private mortgage insurance premiums. This insurance protects the lender should you default on the loan. Premiums are added to your monthly payment.

When financing a house, giving a large down payment will result in a lower mortgage rate. This is due to the fact that a big down payment will reduce your loan to value ratio. When the loan to value ratio gets lower, the interest rates become more favorable for the home buyer.

Make sure you've got all of your paperwork in order before visiting your mortgage lender's office for your appointment. While logic would indicate that all you really need is proof of identification and income, they actually want to see everything pertaining to your finances going back for some time. Each lender is different, so ask in advance and be well prepared.

If you struggle to get a type of mortgage from a credit union or bank, try going with a broker. A mortgage broker can usually find a lender who might be able to work with someone that fits your criteria. They do business with a lot of lenders and can give you guidance in choosing the right product.

If you have bad credit, avoid applying for a home mortgage. Although you may feel financially ready enough to handle the costs of a mortgage, you will not qualify for a good interest rate. This means you will end up paying a lot more over the life of your loan.

Choose your mortgage lender many months in advance to your actual home buy. Buying a home is a stressful thing. There are a lot of moving pieces. If you already know who your mortgage lender will be, that's one less thing to worry about once you've found the home of your dreams.

Investigate preapprovals before you start home shopping. Preapproved mortgages will give you an idea of both how much home you can afford plus what your monthly mortgage payments will be. This will set the parameters of your home shopping and save you time not looking at properties you can't realistically afford.

Avoid interest only type loans. With an interest only loan, the borrower only pays for the interest on the loan and the principal never decreases. This type of loan may seem like a wise choice; however, at the end of the loan a balloon payment is needed. This payment is the entire principal of the loan.

Look into foreclosed homes before you seek out properties that are brand new. Banks don't mind dealing with other banks, and they certainly prefer less expensive properties. If you can find a home that's offered for a great price, especially if the bank in question owns it, they will jump at the opportunity to have someone pick up the tab. It's a better option for them than auctions.

Shop around for a mortgage broker that is a good fit for you. Remember that you are about to embark on a decades-long relationship with this lender, so you want to feel entirely comfortable dealing with the company. Do some online research, read reviews, look for lenders with excellent BBB ratings. Once you have sorted out a few, call and/or visit their offices. Apply with them and see if you can get a letter of pre-approval from the lender you eventually settle on.

Look into a mortgage that requires payment every two weeks as opposed to monthly. This will let you make more payments every year, greatly reducing the amount of money you spend on interest on the life of the loan. This works well if your pay period is every two weeks since the payments can be automatically drawn from your bank.

When shopping for a mortgage loan, ask if the rate is adjustable or fixed. Adjustable rate loans have interest rates which can vary greatly during the life of the mortgage. Also, your monthly payments will never be fixed and can increase by hundreds of dollars monthly. If the rate on the loan is adjustable, ask how and when the loan payment and rate could change.

The more you know about home mortgages, the better off you'll be when it's time to sign the papers. By using tips like the ones provided to you above, you can avoid a lot of the traps and scams that snag so many others. Just take your time, learn about the subject, and never sign anything unless you understand it.